%20Ltd_Gold.png)

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

What First-Time Homebuyers Actually Need to Qualify for a Mortgage in Canada (Without Losing Their Mind)

GUEST BLOG by Ashleigh Holtman, Mortgage Broker

First-Time Homebuyer? Let’s Make Mortgage Rules Make Sense

Being a first-time homebuyer in Canada is exciting… right up until you start Googling mortgage rules and suddenly feel like you need a finance degree, three calculators, and a stiff drink.

Let’s simplify this.

Because qualifying for a mortgage is not nearly as mysterious as it feels online—and it’s definitely not as scary when you actually break it down properly.

First, Let’s Clear Up Two Big Myths

There are two things I hear constantly from first-time buyers:

- “I need 5% down on the whole purchase price.”

- “I just need the lowest rate and I’m good.”

Both are confidently said… and both are usually wrong.

The down payment rule especially loves to trip people up. For example, if you’re buying a $650,000 home, the 5% doesn’t apply to the entire purchase price the way most people assume. There’s a tiered structure in Canada that often changes the math.

I recently had a client ready to go with 5% saved, feeling very responsible and mortgage-ready. Then we ran the numbers together… and suddenly the spreadsheet became the villain in the story.

Nothing was wrong—they just didn’t know how the rules actually work. Which is very normal, by the way.

The Mortgage Chair (Yes, This is a Thing Now)

I use a “mortgage chair” analogy with clients, and once you hear it, you can’t un-hear it.

Your mortgage application sits on top of a chair supported by four legs:

- Credit

- Income

- Down payment

- Property

If all four legs are strong, the chair is solid. Everyone’s happy. Mortgage gets approved. Life continues.

But if one leg is weaker—say your credit score isn’t perfect—the chair doesn’t collapse. It just gets a little wobbly.

If we start removing too many legs at once… like a new job, higher-risk property, or limited savings—then we’ve got a chair situation that even IKEA wouldn’t approve of.

The good news? We usually don’t throw the chair out. We adjust it.

What Lenders Actually Care About (In Normal People Language)

Let’s translate the “official” version into reality:

Credit

Not perfection. Just proof you’ve handled debt without chaos. Think “responsible adult energy,” not “financial superhero.”

Income

Can you actually afford this mortgage without surviving on instant noodles and hope? Stability matters more than just the number.

Down Payment

Yes, you need one. No, it’s not always just 5% on everything. And yes, gifted funds or structured savings can sometimes help.

Property

The house also has to make sense. Lenders are funny like that—they like homes that aren’t falling apart or wildly overpriced for the area.

What If You Don’t Qualify Right Away?

Here’s the part people don’t always expect:

Most mortgage files are not “approved” or “declined” on first glance.

A lot of them are more like:

“Not today… but here’s your plan.”

Depending on the situation, we might:

- Clean up credit over a short period

- Adjust purchase price expectations

- Time things better with employment changes

- Explore different lender options

- Restructure how the down payment is being used

It’s rarely a dead end. It’s usually a detour.

The Bank Myth (Let’s Talk About It)

This is the one I always gently push back on.

Going directly to your bank does not automatically mean:

- Better rate

- Better approval

- Better advice

Sometimes it works out that way. Sometimes it absolutely doesn’t.

Banks offer their products. Mortgage brokers work across multiple lenders and strategies to find what actually fits your situation—not just what fits their shelf.

And yes… sometimes the difference is more than just a few basis points. It’s whether the deal works at all.

The Big Truth About Buying Your First Home

If I could leave every first-time buyer with one thing, it’s this:

You don’t need to “figure it all out” before talking to someone.

You just need to understand the basics—and then get a plan built around your actual situation.

Because no two applications are the same, even if they look similar on paper.

That’s where the real work happens.

Want to See Where You Stand?

If you’re thinking about buying your first home and want to know what the numbers actually look like for you, you can check out more here:

C: 250-365-9516

E: ashleigh@holtmansmortgages.ca

W: holtmansmortgages.ca

No pressure. No guessing. No spreadsheet panic required.

What “MLS® Exposure” Really Means (and why it matters)!

If you’ve ever thought about selling your home, you’ve probably heard the term “MLS exposure. But what does that actually mean… and why does it matter so much?

What is MLS®, really?

The Multiple Listing Service (MLS) isn’t just a website, it’s a powerful system used by realtors (over 29,000 in BC alone)!! to share listings with each other and connect buyers to homes.

When your home is listed on MLS, it doesn’t just sit in one place. It’s instantly distributed across:

- Realtor platforms

- Agent databases

- Buyer “matched searches”

- Public websites like Realtor.ca

It’s the difference between quietly posting your home on Facebook Marketplace… and putting it in front of everyone who’s actively looking.

How buyers are actually searching

Serious buyers are set up on custom searches through their agent.

That means:

- They get instant alerts the moment a home matching their criteria hits MLS

- They’re seeing your property within minutes or hours – not days

- They’re often ready to book a showing right away

These are your most motivated buyers. Without MLS exposure, you’re missing them entirely.

Why exposure = better results

The more people who see your home, the more opportunity you create. And in real estate, that matters because:

- More eyes = more showings

- More showings = more interest

- More interest = stronger offers

Sometimes, it’s not just about getting an offer – it’s about creating the kind of demand that gives you leverage in negotiations.

The risk of limited exposure

With “off-market” or private sales, you’re limiting your audience.

That can mean:

- Fewer buyers competing

- Less urgency

- Potentially leaving money on the table (even with commissions to consider).

Because the right buyer… might never even know your home was for sale.

MLS® is powerful but it’s not magic on its own 🙋🏼♀️

How your home is presented within that system matters just as much:

- Pricing strategy

- Professional photos and engaging video (MY SPECIALTY 🎥)

- Description and storytelling (also love this part)

That’s where a thoughtful approach really makes the difference between just being listed and standing out.

The bottom line

Your home is one of your biggest assets.

Giving it the right exposure isn’t about “doing more” – it’s about making sure the right buyers see it at the right time.

Because when that happens, everything else such as showings, offers, and negotiations, gets a whole lot easier.

If you’ve been thinking about selling and want to understand what your home could look like on the market (and how to position it properly), I’m always happy to walk you through it!

No pressure, just a conversation ☺️

LISA NICOLE

Taking You From One Stage To The Next

📲 778-554-9289

📧 lisa.nicole@century21.ca

Serving the West Kootenay’s

Trail-Rossland-Castlegar-Christina Lake-Grand Forks-Nelson-Warfield-Fruitvale

Will Mortgage Rates Go Down in 2026? Here’s What You Need to Know

GUEST BLOG by Ashleigh Holtman, Mortgage Broker: Will Mortgage Rates Go Down in 2026? Here’s What You Need to Know

One of the most common questions I get from clients is: “Will mortgage rates go down?” It’s a fair question. Rates have been fluctuating recently, influenced by inflation, global events like the conflict in Iran, and overall economic uncertainty. Many people worry about overpaying for their mortgage or making a move at the wrong time. The truth is, while we can analyze trends and make educated guesses, no one can predict rates with certainty.

From my experience, trying to time the market rarely works. I always tell my clients: buy when you’re ready. Your finances, your life situation, and your comfort level should dictate the timing of your purchase – not trying to chase the “perfect” interest rate. Waiting for rates to drop can backfire, sometimes costing thousands more in interest if rates rise instead.

I’ve seen this play out firsthand. A client of mine was ready to put in an offer, and we went through several different scenarios together. I suggested putting in a rate hold to lock their rate, but they declined. A few weeks later, rates went up, and because they waited, both their interest rate and their monthly payment increased. That experience reinforced a key lesson I share with every client: readiness beats timing.

To make this even clearer, let’s break it down with a scenario using a minimum down payment, including mortgage default insurance:

- Home price: $500,000

- Minimum down payment: 5% ($25,000)

- Mortgage amount: $475,000

- Mortgage default insurance (CMHC ~4.0%): $19,000

- Total mortgage including insurance: $494,000

- Initial rate offered: 3.99%

- New rate if waiting a few weeks: 4.39%

-

Monthly payment: ~$2,350

-

Monthly payment: ~$2,460

That’s about a $110/month increase – or over $6,500 more in payments and $9,400 more in interest over a 5-year term.

And this is exactly my point: even a small shift in rates can have a meaningful impact, especially when you’re purchasing with a minimum down payment and financing a larger amount.

Another misconception I encounter constantly is that the lowest rate is the best rate. This isn’t true. Your mortgage needs to work for your life, your budget, and your goals. Sometimes a slightly higher rate comes with flexibility, better terms, or options that actually save you money long-term. The “best” mortgage is the one that fits your situation – not just the one with the lowest percentage.

Looking ahead in 2026, there are a few factors to watch. Inflation is a big one. If it continues to rise, the Bank of Canada may raise its overnight rate to control it, which would put upward pressure on variable rates. Fixed rates, on the other hand, are driven by the bond market and can move quickly based on economic expectations and global uncertainty.

The reality is, rates may go down – but they may also go up before they do. And trying to wait for the “perfect” moment often leads to missed opportunities or higher costs.

So what does this mean for you? Focus on what you can control. Your income, your budget, your comfort level, and having a solid plan in place. Get pre-approved, understand your options, and make a decision based on your readiness – not headlines!

In the end, 2026 will bring movement in rates. It always does. But the clients who do best aren’t the ones who perfectly time the market, they’re the ones who are prepared and make informed decisions when the timing is right for them.

Ashleigh Holtman with Mortgage Architects

C: 250-365-9516

E: ashleigh@holtmansmortgages.ca

W: holtmansmortgages.ca

What “Subject to Sale” Means for You This Spring

Subject to sale is common this time of year – and strategy matters!

THE STRONGEST POSITION 💪🏻 you can be in as a buyer is having your home already listed (or even better, sold) before you start house shopping or put in an offer!

This gives you a clear understanding of your price point, strengthens your negotiating power, and makes your offer far more attractive to sellers. If you do not have the “Subject to Sale” condition, a seller is far more likely to work with your offer over one that does.

This is important in the Spring market as we see far more multiple offer scenarios!

The weaker position is finding a home first, which can put you in a rushed, pressured position – either scrambling to list quickly or risking losing the property altogether. Doing it this way means you’ll need the “Subject to Sale” condition, and that allows the seller to add a time clause and continue entertaining other offers. When another offer comes in that the seller wants to accept, you have 48-72 hours to remove ALL conditions, including the sale, which is nearly impossible in that short amount of time.

Key takeaways 👇🏻

• List first = stronger negotiating position

• Cleaner offers are more attractive to sellers

• Subject to sale = added pressure and risk

• Time clauses can put you on the clock and losing your dream home!

There’s more to it, but that’s the short of it! Listing first puts you in control, not the market.

LISA NICOLE

Taking You From One Stage To The Next

📲 778-554-9289

📧 lisa.nicole@century21.ca

FREE Movie! Zootopia 2 at The Royal Theatre Sunday Feb 22nd.

Centurion Award in Trail, BC

West Kootenay Real Estate Agent Centurion Award

This Centurion Award isn’t just mine — it belongs to every client who trusted me with one of the biggest decisions. And wow, it’s based on the TOP 7.4% of Century 21 realtors in Canada!

Thank you for choosing me, and letting me be in your corner. I don’t take that lightly. 💛🏡

Here’s to continuing to raise the bar in 2026 🥂

What matters most for you in an agent?

LISA NICOLE

Taking You From One Stage To The Next

📲 778-554-9289

📧 lisa.nicole@century21.ca

Serving the Kootenay Boundary region: Trail – Castlegar – Rossland – Fruitvale – Warfield – Salmo – Grand Forks – Christina Lake

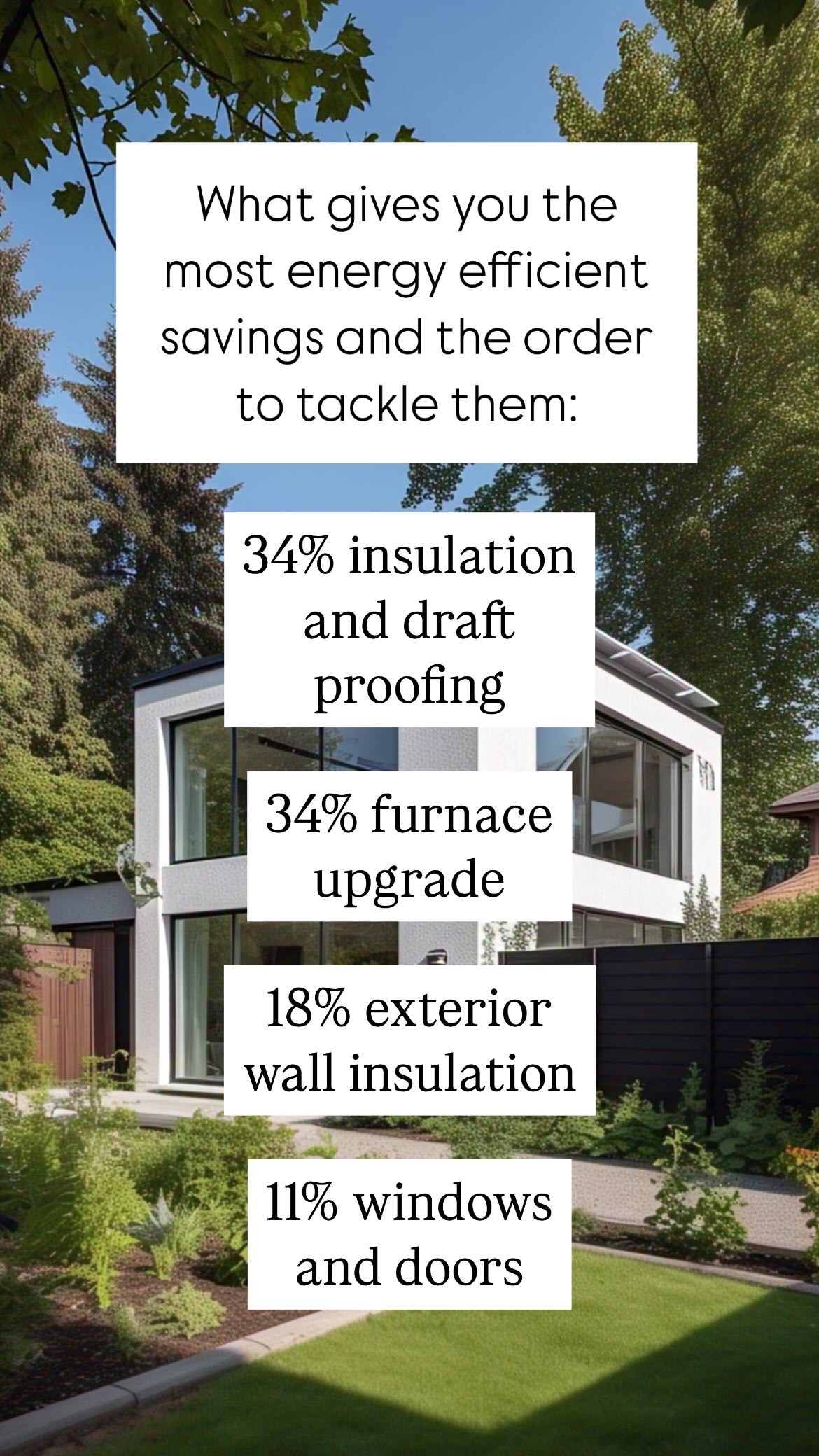

Energy Conservation & Savings

Energy efficiency improves your comfort level and increases a building’s profitability and savings!

The major factors that affect energy consumption and conservation are the building structure & the HVAC system.

Start with your insulation and draft proofing and end with updating windows and doors!

Here is a local HVAC company to reach out to for questions or quotes!

Lisa Nicole

Taking You From One Stage To The Next

📲 778-554-9289

📧 lisa.nicole@century21.ca

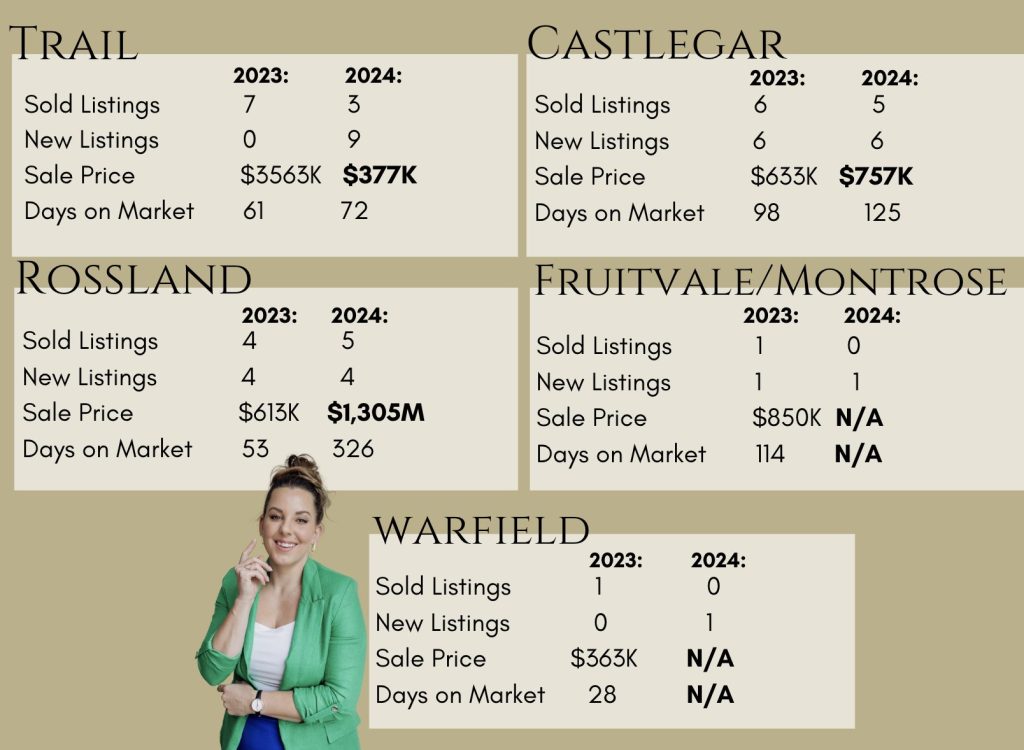

December Market Update West Kootenay’s

A Market Update On Single Family Homes!

Bank of Canada reduces policy rate by 50 basis points to 3.25%

The Bank of Canada has announced it’s final reduction in its policy interest rate this year, cutting it by 50 basis points! Getting closer to the 2% target.

Here’s a breakdown of the rationale behind this decision and its potential impacts:

What does this mean?

- Lower interest rates are starting to stimulate housing activity, signalling a busy Spring market ahead!!

- Lower interest rates are good news for variable-rate mortgage holders and those considering refinancing or new financing options.

The next rate decision is January 29, 2025!

Lisa Nicole

Taking You From One Stage To The Next

📲 778-554-9289

📧 lisa.nicole@century21.ca

Selling Your Home? Avoid These 3 Common Mistakes! 🚫🏡

Mistake 2: Neglecting Home Presentation

Mistake 3: Inadequate Marketing

Ready to list? Contact me today ☺️

Lisa Nicole

Taking You From One Stage To The Next

📲 778-554-9289

📧 lisa.nicole@century21.ca