%20Ltd_Gold.png)

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

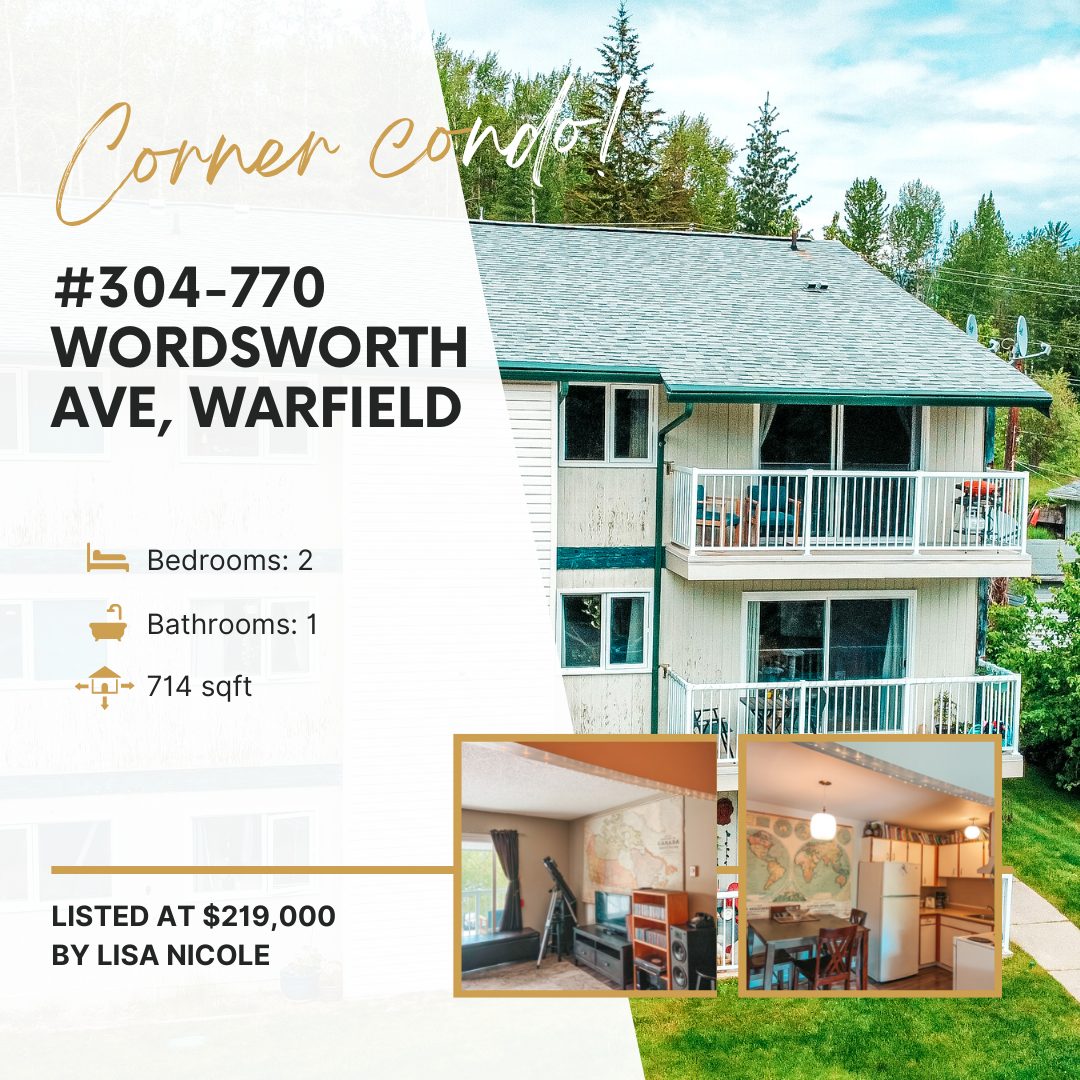

✨ NEW LISTING 📍 #304-880 Wordsworth Avenue, Warfield

Click HERE to view listing!

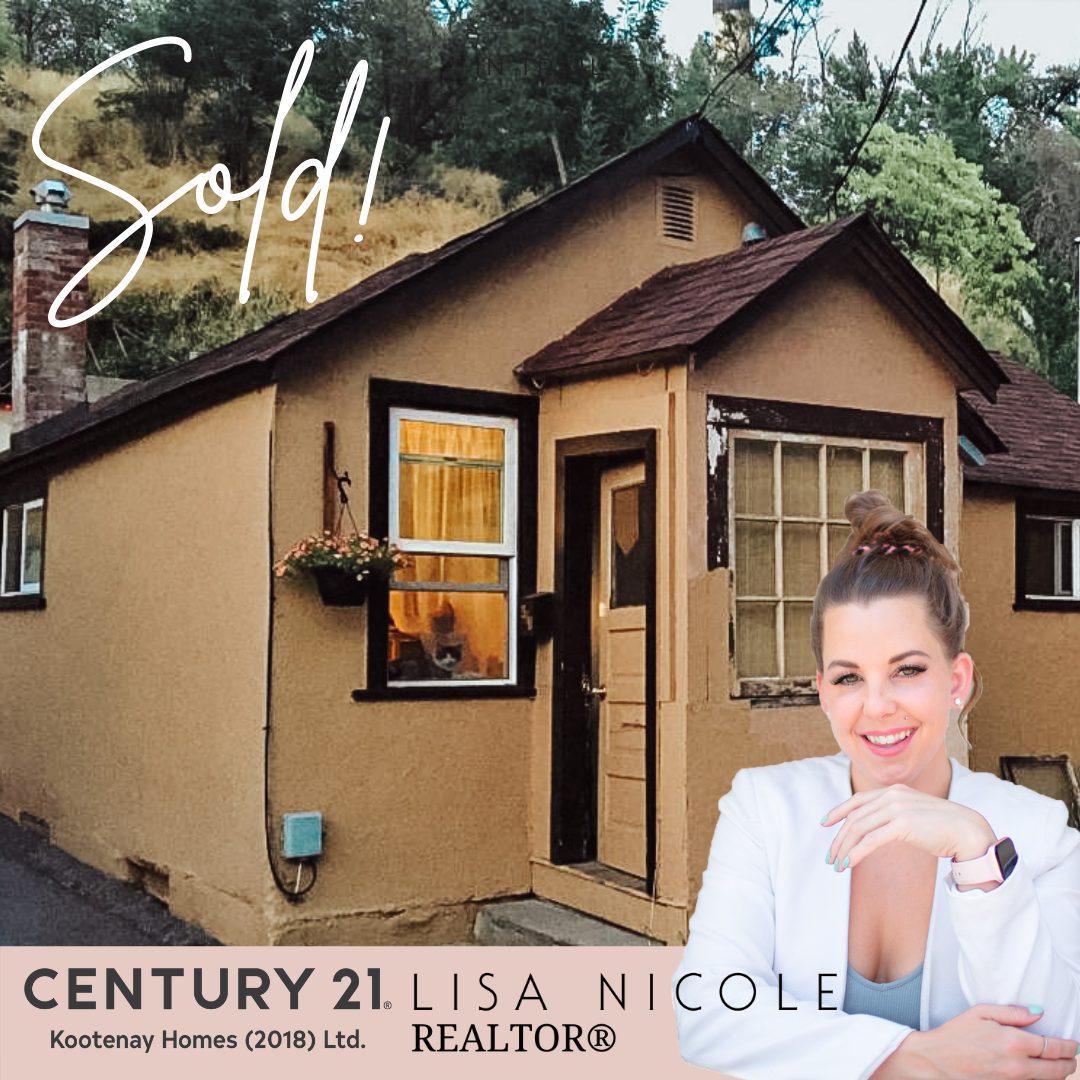

SOLD SOLD SOLD!

Happy Spring 🌷 How happy are you that the snow has melted in your yard and warmer temperatures are in the forecast! It’s no surprise we’re starting to see more homes pop on the market this time of the year, but inventory is still incredibly low. In February we had around 13,000 active listings in BC – almost a record low! Whereas a healthy level is around 40,000!

Happy Spring 🌷 How happy are you that the snow has melted in your yard and warmer temperatures are in the forecast! It’s no surprise we’re starting to see more homes pop on the market this time of the year, but inventory is still incredibly low. In February we had around 13,000 active listings in BC – almost a record low! Whereas a healthy level is around 40,000!

There is a strong demand for real estate. There are many qualified buyers that are ready, willing and able to purchase.

Let’s get your home on the market so you can see it SOLD just like these!

Lisa Nicole

Taking You From One Stage To The Next

C: 778-554-9289

E: lisa.nicole@c21.ca

QUESTIONS TO ASK WHEN HIRING A REALTOR

Choosing the person to trust with one of your biggest monetary assets, your home, is a big decision. Be prepared by asking a few important questions to make sure that the agent is right for you and has the experience and skill set to get you to the closing table!

QUESTIONS TO ASK WHEN HIRING A REALTOR:

How will you market my home?

Make sure that your listing agent doesn’t plan to list your home by simply uploading it to the MLS & pray someone brings a buyer. That is almost never enough. Ask about their marketing plan & make sure that it makes sense to you! Don’t be afraid to ask questions.

How will you market my property online?

I hate to say it, but some agents are still sticking a sign in the yard, and calling it a day. No thanks. Over 90% of buyers are looking online for homes at some point during their search. If your agent isn’t utilizing digital marketing along with social media then you are losing out on a very large pool of buyers.

Will you hire a photographer?

Do some online research. See that home with the agent in the mirror, taking a picture of the bathroom with the toilet seat up? It’s getting less views, which means less showings, which means it will be on the market longer, potentially resulting in it selling for a lower price. That’s a pretty big downward spiral don’t you think? Make sure your agent hires a professional photographer so that your home stands out & looks it’s best!

What is your experience in general?

See what their background is and what skill set they are bringing to the table. While real estate experience is important, having a professional background in other things can be a great way to round out their experience.

Do you have another full time job?

While I respect the hustle, it’s important that your real estate agent’s focus is on you and your home! If they are only moonlighting as an agent, their focus is going to be limited and it can potentially effect their performance. In addition, there may be some times that they are unavailable to provide the service you hired them for since they will be working another job. Hire a full time, dedicated real estate professional.

If I list with you, will you be the person I deal with?

Make sure the person you are speaking with will be the person you will work with. Some agents have additional staff that they pass their listings or buyers on once the contract gets signed. While having a support team is great, hiring one person but never being able to communicate with that person is another.

How often do you communicate?

Selling your home is stressful! You should never be left guessing what is happening with the sale of your home. Make sure that your agent has systems in place to keep you up to date on what they are doing to get your home sold. Once your home is under contract, there are lots of details that need to be done & deadlines that need met. Your agent should keep you on track & communicate with you often!

What is your negotiation style?

Real Estate is a team sport – everyone has to work together to get to finish line. While your agent should always have your best interests in mind, it’s important they play well with others. Being bull headed and hard to deal with can often lead to lost deals & lose you lots of money! On the other side of that coin, your agent should be able to stand their ground when it matters.

How much should my home be listed at?

Are you ready for the most shocking answer of all? You should not just list with an agent who brings you the highest number & call it a day. Wait, what?!? While a higher number is tempting, remember that buyers will only pay what the market says your home should be valued at. And most of the time, buyers won’t pay anything higher than the appraised value of your home. What your home should be listed at should be based on multiple factors. Your agent should do research and be able to show you why & how they came up with the numbers for your home. Be wary of an agent who brings high numbers with no data backing it up – you’ll end up with your house on the market for too long, resulting in it actually selling lower than what it would have if it was priced correctly to being with!

Why should I hire you?

Bottom line is no two agents are the same. Make sure that you are able to connect & build rapport with the real estate agent you are interviewing. Ask what makes them different from all the other hundreds or thousands of agents in your town. If at the end of the interview you have doubts or don’t feel confident that they are the right agent for you, listen to your gut! It’s okay to “no thanks” and interview someone else!

Buying or selling a home is a huge financial and emotional event and it’s important that your agent is able to confidently help you navigate the transaction.

Need help finding a real estate professional in your area? I have a huge network of amazing agents all over the country and would love to help you find one that is perfect for your needs! Reach out to me & I can provide you with a list of agents you can interview in your area.

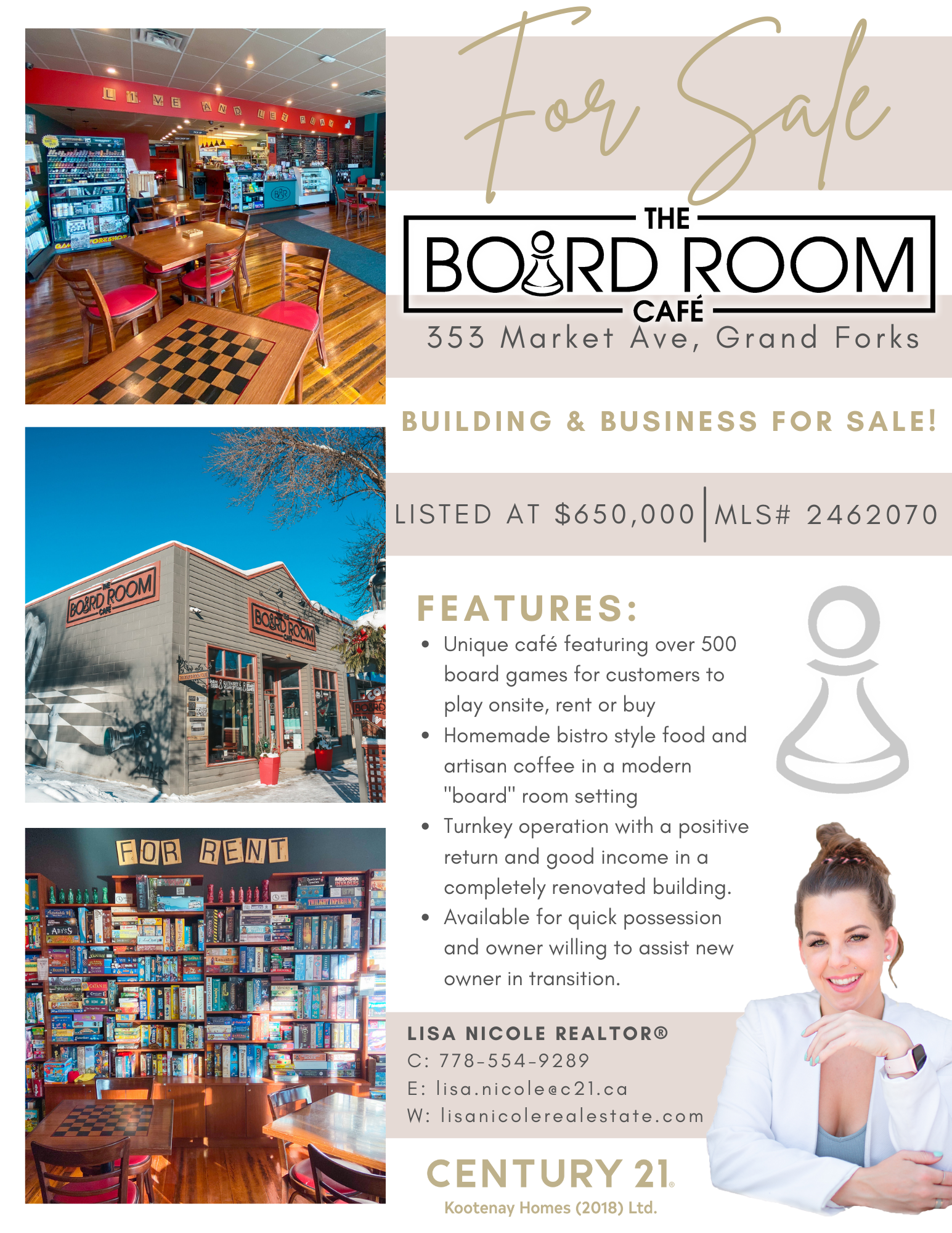

The Board Room Cafe is FOR SALE!

Located in the heart of Grand Forks, BC, is the region’s first board game cafe with loyal local clientele and a Summer tourist attraction. The Board Room Cafe is well known for, well, their board games! Along with their fantastic, freshly made food including vegan options, plus their delicious beverages! Although board games are their niche, the majority of their sales and the reason they are frequented is primarily from their food and drink.

Customers purchase memberships which allow them access to the game library. Memberships are regularly renewed and clients also purchase food and drinks while they stay and play! Business also includes a liquor license.

The Board Room Cafe has experienced staff and systems in place with current owners prepared to assist the transition of the new cafe owners.

The sale includes the building and a full line of equipment and game inventory. The 2000 sqft building sits on a .086 size lot with room for parking in the back. The same space out back could be used to add onto the building as there is ample parking on the side.

A turn-key operation! Providing good income and a substantial client base as well as additional opportunities to grow.

Get on board this building and business and contact your REALTOR® today!

353 Market Avenue, Grand Forks | Listed at $650,000 | MLS® 2462448

👇🏻 TAKE THE VIRTUAL TOUR 👇🏻

WWW.THEBOARDROOMCAFE.CA

Seller FAQ!

Here are some seller frequently asked questions!

Selling a house is a big undertaking. And if you want to ease the process while also maximizing profits, then being prepared is key.

Are you thinking of listing your house in the near future? Make sure you ask yourself these important questions before moving forward.

Q: When is the best time of year to sell a house?

A: You can sell your home at any time of the year, but there are definitely some months (and even specific days) when selling is easier, faster, and more profitable. Peak selling seasons vary from year to year in most market places and weather usually has a lot to do with that. Often early spring and early fall are the prime listing seasons as houses tend to “show” better in those months than they do in the heat of summer. Be aware that there are also more houses on the market during the prime seasons, resulting in more competition. While seasonality is a factor, it’s not something that should dominate your decision on when to sell. Winter has it’s upsides such as a low inventory. When you’re the only home for sale in the neighbourhood, your chances of selling are pretty good!

Q: How in-demand is real estate in my area? Is it a buyer’s market or a seller?

A: Real estate is in high demand in the Kootenay’s. We’ve seen quite the spike in real estate when the pandemic hit. Work from home became popular, which meant you didn’t have to live in the city to do your job.

You’ll maximize profits and minimize your home’s time on the market if you list it in a seller’s market.

Q: What are local market conditions?

A: You might consider gauging local market trends like the number of active listings or median sale price before deciding to list your home. Every month I release local real estate statistics – sign up HERE for my newsletter to receive them!

Q: How long will it take to sell my house?

A: Time to sell really depends on where you’re located, the conditions of your local housing market, your listing price, the condition of your home, and you (or your agent’s) marketing and staging prowess can also play a role. Currently the average days on the market for single family homes is 62 days, and 55 days for multi family homes.

Q: How much does it cost to sell my house?

A: There are many costs involved in selling a house. Fortunately, most of them don’t require an out-of-pocket payment, such as the real estate commission. Many come out of your sales proceeds at closing.

Q: Should I make repairs before listing the house?

A: Many times, homebuyers want a “move-in ready” property — one that doesn’t require much work and elbow grease before moving in. This is especially true of younger buyers, 76% of whom say a move-in ready home is a must. For this reason, you may want to consider making some repairs before putting your home on the market. Smaller, cosmetic repairs can be a good idea to make your home more marketable (and more valuable).

Q: Can I take my favourite light fixture (or other favourite home feature) with me?

A: Anything that’s attached to the house is something you’ll need to leave behind for the buyer. This includes light fixtures, built-in shelving units, blinds, door hardware, and more. If there’s something specific you don’t want included in the sale, make sure you bring it up during negotiations. You’ll need to note it in your sales contract.

When you are thinking to list your home, contact me for a complimentary market evaluation and staging advice!

C: 778-554-9289

E: lisa.nicole@century21.ca

What is an appraiser and do I need one?

What is an appraiser?

Appraisers are licensed or certified professionals who provide a qualified, unbiased opinion of value. Appraisers are required to be licensed or certified to provide appraisals to federally regulated lenders. Meaning, you’re working with a highly trained individual who understands current real estate market conditions in your area.

Appraisers are considered third-party participants in the transaction. Their work assures mortgage lenders that the amount they are lending does not exceed the home’s true value. Yet, it also assures that you (as the home buyer or homeowner) are receiving a fair, unbiased price for your property.

What does a home appraiser look for?

The appraiser researches recently sold properties in your area with features similar to your prospective home, called “comparables.” Comparables are sales records of recently sold homes. Appraisers and real estate agents use at least three comparables, usually through the Multiple Listings Service (MLS), to get the most accurate estimate possible of a home’s value. The three comps must be sales that have closed within six months of your appraisal date to be considered accurate.

You can expect the following factors to be reviewed:

- The condition of the home (are there any cracks, damages, leaks, etc.)

- The size of the home and the property lot

- The quality of landscaping

- The quality of roofing and foundation

- The number of bedrooms and bathrooms

- The quality of lighting and plumbing

- The number of fireplaces

- The condition of a swimming pool or sprinkler system

- The quality of the basement (whether it’s finished or unfinished)

- The finishing details in the home (such as granite countertops, hardwood floors, and appliances)

A home appraisal is not the same as a home inspection. Learn about the differences and the importance of home inspections.

How long does an appraisal take?

For home buyers or borrowers looking to refinance: you can expect an appraiser to be at your home from 30 minutes to two hours, depending on the size of the property. They’ll use that time to take photos of all areas of the home which will document the condition of the home.

Once the physical appraisal is complete, the appraiser creates a written report of findings for the mortgage lender. This generally takes three to five days. The appraiser must confirm all data, so this takes some time.

How to prepare:

Maximize your home value ahead of time, so your home appraises as high as it can. This may include significant work such as home renovations, or simple tasks like the ones listed in the checklist below:

Appraisal checklist for selling or refinancing a home:

- Ensure your landscaping is on point as “curb appeal” is considered during an appraisal

- Repairing damaged drywall or painting rooms can factor into your valuation

- Make sure every light switch, wall outlet, fan or vent works

- Document recent home improvements with estimated prices and dates

- Provide copies of previous appraisals

- Make sure all rooms of the house are accessible

- Be flexible and coordinate the appointment around the appraiser’s schedule

- Let the appraiser do the inspection without distraction

Be aware of the $500 rule!

Appraisers tend to value property in $500 increments – like $300,000, $300,500, $301,000, etc. Because appraisals with $500 increments are common, it’s in your best interest to make small repairs if you are selling your home or refinancing. Even the smallest of changes can contribute to the overall condition of your property.

For any real estate questions – do not hesitate to reach out to me!

C: 778-554-9289

E: lisa.nicole@century21.ca

Home Staging Tips

Here are some of my staging tips to help sell your home in the best possible light!

Start With Curb Appeal

First impressions matter, so make your home stand out the instant buyers pull up to the curb. Some upgrades can be done in a weekend and will cost more in sweat equity than actualdollars. A few suggestions: rent a pressure washer to remove dirt and grime from your siding, roof, fascia, and gutters. Paint the front door and/or shutters a bright color, but make sure it coordinates well with the rest of the home’s colors. Replace old house numbers, lighting, the mailbox, and welcome mat. Clean up the edging around flowerbeds and lay down fresh mulch. Fill in empty beds with small shrubs, seasonal flowers, and greenery. Even if it’s the dead of winter, get a pair of urns or large planters and fill them with small evergreen shrubs and cold-hardy annuals. If you have window boxes, fill them with fresh greenery too. If your porch or stoop has room for furniture, add a couple of chairs to expand your outdoor living space.

Give the Kitchen a Facelift

Kitchens sell houses, so any updates you make have the potential to go a long way. And they don’t have to be expensive; some upgrades can be accomplished with mostly elbow grease. Start by showing off your storage. Pack up the seldom-used small appliances and holiday dishware for your next house and use up all the dry goods in the back of the pantry. Clear clutter off the countertops. Consider giving your cabinets a facelift with paint; go for classic white or try a dark neutral like gray or slate blue. At the very least, change the outdated hardware for an easy DIY. A corroded faucet or one caked with hard-water stains can be a big turn-off; swap it out for one with style and added function. Instead of replacing the dishwasher, check with the manufacturer to see if they sell replacement panels for your model. If not, peel-and-stick contact paper can be used to make your dishwasher and your other appliances look like stainless steel. To update a backsplash on the cheap, try peel-and-stick faux tile, tin tile, beadboard paneling or try painting the existing tile.

Pare Down Furniture

The most important thing you can do to prepare your home for sale is to get rid of clutter. One of the major contributors to a cluttered look is having too much furniture. When professional stagers descend on a home being prepped for market, they often whisk away as much as half the owner’s furnishings, so the house looks bigger. You want potential buyers to be able to move around each room without being blocked by furniture. Make sure they can easily access your home’s best features like the fireplace or built-in bookshelves, and make sure they can look out all the windows. Avoid a cluttered look by minimizing items on the coffee table and not piling so many pillows on the couch that nobody can sit on it.

Rethink Furniture Placement

There’s a common belief that rooms will feel larger if all the furniture is pushed against the walls, but that isn’t the case. Instead, furnish your space by floating furniture away from walls. Reposition sofas and chairs into cozy conversational groups, and place pieces so that the traffic flow in a room is obvious. Not only will this make the space more user-friendly, but it will open the room and make it seem larger.

Add Functional Office Space

These days more people are working from home and homeschooling is becoming commonplace, so a workspace may be essential for your potential buyers. If you don’t have an entire room to dedicate to a home office, carve out a nook in a spare bedroom, a corner of the living room or even a closet.

Depersonalize

Potential buyers want to be able to picture themselves in your home, and that’s hard to do if all they see are your personal items. Remove family photos, your kids’ artwork, framed diplomas, and personal collections. Pack these items up to take to your new home and replace them with generic artwork.

Show Off Your Storage

Storage always ranks high on buyers’ priority list. Show off yours by decluttering your closets and cabinets. Keep closets neat by stashing items in matching baskets and cloth bins. Implement shoe racks and under-shelf baskets to demonstrate the versatility of your storage. Straighten out the linen closet and add a couple of satchels of potpourri so when buyers peek inside, they’ll be greeted by fresh-smelling sheets and towels.

Make Bathrooms Shine

Scrub the bathrooms, then scrub them all again. Nothing is going to turn off a potential buyer more than a scuzzy bathroom. Remove hard-water stains from faucets, make sure there is no sign of mold and remove clutter by whittling down your cosmetics and products in the vanity and medicine cabinet. Invest in new shower curtains, rugs, and bathmats (you can always take them with you when you move). If the tile is looking old, consider having it repainted. If discolored grout is an issue, you can fix that with a $15 bottle of grout stain. If there’s moldy caulk around the tub or shower, remove it using a razor blade then recaulk the entire area. Then when all that cleaning is done, create a spa look with fluffy white towels, candles, a few fancy soaps, and a couple of apothecary-style accessories.

Amp Up the Lighting

One of the things that make staged homes look so warm and welcoming is great lighting. Increase the wattage in your lamps and fixtures. Aim for a total of 100 watts for every 50 square feet. Don’t depend on just one or two light fixtures per room, either. Make sure you have three types of lighting: ambient (general or overhead), task (pendant, under-cabinet or reading) and accent (table and wall).

Erase Signs of Pets

We totally understand how much you love your pets (we do, too), but potential buyers may be turned off by pet odors or be allergic to fur and dander. Thoroughly clean the areas where your pets spend most of their time and add air fresheners. When potential buyers come calling, throw the pet beds, crates, toys, food dishes and litter boxes in your car then take Fido or Fluffy for a walk in the park.

When should you invest in real estate?

Don’t wait to buy real estate, buy real estate and wait. Real estate investing is not about timing the market. It’s about your time IN the market 📈.

There is never going to be a perfect time. A lot of people may try to time the bottom of the market but no one knows when they are in the bottom until after the fact. Those that look for reasons not to act will soon be saying that prices are falling so they don’t want to invest. Or that interest rates are too high. Quote me on this.

How many times have you heard someone say:

🕰️”I’ll just wait until the market slows down, it’s too unstable”

📉”Mortgage rates are too high”

💸”The market is going to crash, I’ll wait and buy then”

And more then likely, you’ve heard this:

🏡”I should’ve bought that house ____ years ago”

🌲”That lot at Red Mountain has doubled in price since ____”

😲”Remember when that house was for sale for $______!”

Instead of obsessing over the best time to buy or sell a property focus on your time IN the market. With a great strategy and realtor by your side you can achieve wealth, a retirement plan, a nest egg for your kids, by investing in real estate now.

👇🏼 What are your thoughts on this market? Let me know! 778-554-9289!

Didn’t you hear?

My monthly real estate newsletter has been a hit so far and it’s set to come out tomorrow!

Sign up for monthly market updates, community events, & featured listings! Just add your details below!

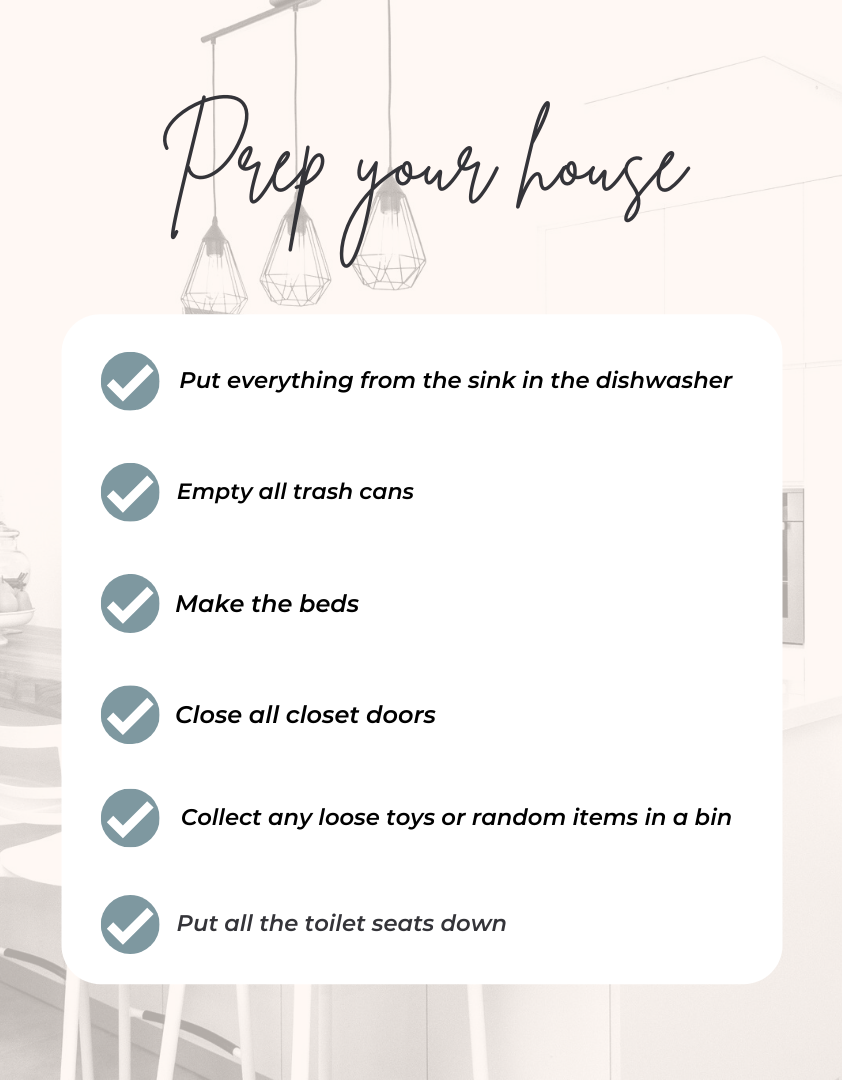

House cleaning tips when selling your home!

I’ve compiled a list of house cleaning tips when selling your home!

Your deep cleaning checklist will help you learn how to clean your house to sell. It will help you to ensure that you don’t forget anything and, importantly, that you pay attention to those items that can be overlooked. If you’re ready to clean your home, you’ll want to start with the big things before you get to the little things.

✔️ The big things

A big part of learning how to clean your house to sell is knowing what the most important parts of your home to clean might be. These are the places and things in your home that are easiest for prospective buyers to spot. If they’re dirty, you can lose a sale. As such, you’ll want to pay special attention to cleaning the following areas.

✔️ The fridge, dishwasher, and oven

These are bigger than you think. While you might be used to how your appliances look and smell, new buyers are going to view them with fresh eyes. You’ll want to make sure they are all cleaned inside and out. There are special products for cleaning out ovens and dishwashers, so invest in those. Make sure that your fridge is emptied and that you’ve cleaned out every shelf and drawer. Put in some extra effort to make sure that each of these major appliances shines.

✔️ The bathtubs, sinks, and toilets

You already know that these are high-traffic areas, so make sure to take care of them appropriately. You’ll need to spend some serious time scrubbing here, removing every stain and bit of stray dirt. Make sure to pay extra attention to both the sinks and bathtubs, as they’re very easy for even casual observers to look into. These are areas in which a little extra effort can go a long way. Empty the garbage cans, no one wants to see trash when viewing a home.

✔️ Glass and mirrors

The goal here is to eliminate all of the streaks and smudges that you can find. Use a good glass cleaner and make sure to leave any glass surfaces as clear as possible. Good mirrors help to make rooms look larger, so you’ll want to make sure that they are clean and that they reflect the light well. Glass also needs to be dusted, as the dust particles can make your entire house look a little bit dingier than it should.

✔️ Walls and counters

Your walls and counters have a few different issues that need to be addressed. First and foremost are the basic marks that have accumulated over the years – a good scrubbing should get rid of most, but don’t be afraid to invest in a special cleaner if you can’t get them out. More pressing is any damage to the walls or counters, which might need to be fixed with either new paint or even putty. Make sure that these areas look as close to new as possible.

✔️ Floors and baseboards

Your floors are the easiest area to see in your home. If they’re not properly cleaned, the rest of your home will look incredibly dirty. Take the time to clean any carpets and use cleaners that you might have on your hardwood floors. You may also need to invest in methods to clean up scratches in some areas. Your baseboards should also be vacuumed and then cleaned by hand in order to get the best results.

✔️ The little things

In addition to the big items, figuring out how to clean your house to sell requires being able to identify the most important little things in your house. These items might not seem like they’d cause problems, but they’re things at which most serious buyers will look before they put in an offer on a home.

✔️ Light fixtures

All of your light fixtures need to be deep cleaned before you move out. This is a multi-part task, so be prepared to put in a little work. Start by removing the lightbulbs so that you can replace if necessary. Next, you’ll want to clean out the inside and outside of the fixtures with a microfiber cloth. Finally, finish by removing any stains and using glass cleaner if necessary. Once you’re done, you can replace the bulbs and you should have not only cleaner fixtures but also much brighter lights.

✔️ Switch plates

Your switch plates tend to accumulate a lot of wear and tear over time. Not only are you constantly switching lights on and off, but you’re also constantly touching the plates without noticing what’s on your hands. It’s very important to examine each individual plate in order to determine exactly how much work you’ll need to do. Disinfectant wipes will help with most, but you may need to replace those that are scratched up. Don’t be afraid to remove the plates in order to make sure that they are clean, as there can often be a fair bit of build-up around the edges of the plates.

✔️ Vents and fan blades

When was the last time you really looked at your vents and fan blades? You might have done a bit of dusting from time to time, but these are areas of the home that tend to get neglected. You’re going to want to remove your vent covers and clean them both inside and out, getting rid of any accumulated dust. If possible, you should also remove each individual fan blade and wipe it down. Make sure that you clean the parts that are generally covered by any lighting fixtures as well so that you can really make the fan shine.

✔️ Hardware

Much like your switch plates, your home’s hardware gets a lot of wear and tear that you probably haven’t noticed over the years. At a basic level, you’re looking to get rid of fingerprints and the kind of random dirt that accumulates over the years. If your hardware is metal, though, you’re going to want to use metal cleaner in order to restore it to its original look. You’re not just dealing with wear and tear here, but very real environmental damage. You’ll need to use a little elbow grease to get the best results and make the hardware look pristine.

✔️ Windowsills

Your windowsills are another area that tends to attract quite a bit of dirt and grime. Unfortunately, most people tend to clean these areas with a light dusting, trusting that most visitors won’t give them a second glance. When buyers come to your home, though, they’ll use your windowsill as a test to see how well you have actually cleaned your home. It’s recommended that you don’t just dust these areas, but that wipe them down and remove any stains. If possible, you may also want to give them a quick coat of paint in order to make them look like new.

🧹 Seems like a lot of work doesn’t it? If you don’t have time to get to it yourself, I have a list of professional house cleaners that range from $25-$35/hour to get the job done!

Otherwise, happy cleaning 🙂